Market Pulse: China’s AI Infrastructure Accelerates — Supercomputing Breakthrough Meets Super-App Talent War

This week, China's AI ecosystem flashed three major signals almost simultaneously: 1. LineShine supercomputer — China unveiled a 1.54 exaflops pure-CPU supercomputer using 2.4 million HiSilicon ARMv9 cores, effectively bypassing the US GPU export ban (Tom's Hardware, May 17). 2. Super-apps go AI-native — WeChat, Douyin (TikTok China), and Meituan are integrating generative AI across their core product lines (The Economist, May 17). 3. "Containment has failed" — The Atlantic (May 18) argues US-China AI capability gaps are narrowing faster than expected, making technology containment strategies increasingly ineffective. Our take: These three headlines converge on a single inflection point — China's AI infrastructure and application layers are accelerating simultaneously. AI talent demand is entering a new super-cycle.

Signal 1: LineShine — The Talent Gravity of Domestic Compute

China built a 1.54 exaflops supercomputer without NVIDIA GPUs. The talent implications are structural:

- Hardware engineering shifts from “buy-and-integrate” to “build-from-scratch”: HiSilicon’s ARMv9 chip design teams are scaling rapidly. Industry estimates suggest chip design roles at HiSilicon now command CNY 850K-1.1M/yr at median, up 18%-22% YoY.

- System software stack is the real bottleneck: Supercomputers aren’t just hardware — compiler optimization, distributed scheduling, and kernel/library engineering roles are in acute shortage. These are not roles that can be backfilled from the general software engineering pool.

Signal 2: Super-Apps Go All-In on AI — Role Restructuring in Real Time

The Economist reports WeChat is embedding an AI copilot, Douyin is rolling out AI video generation, and Meituan is pushing AI-powered recommendation/ordering. This isn’t “adding an AI team” — it’s restructuring every product line around AI.

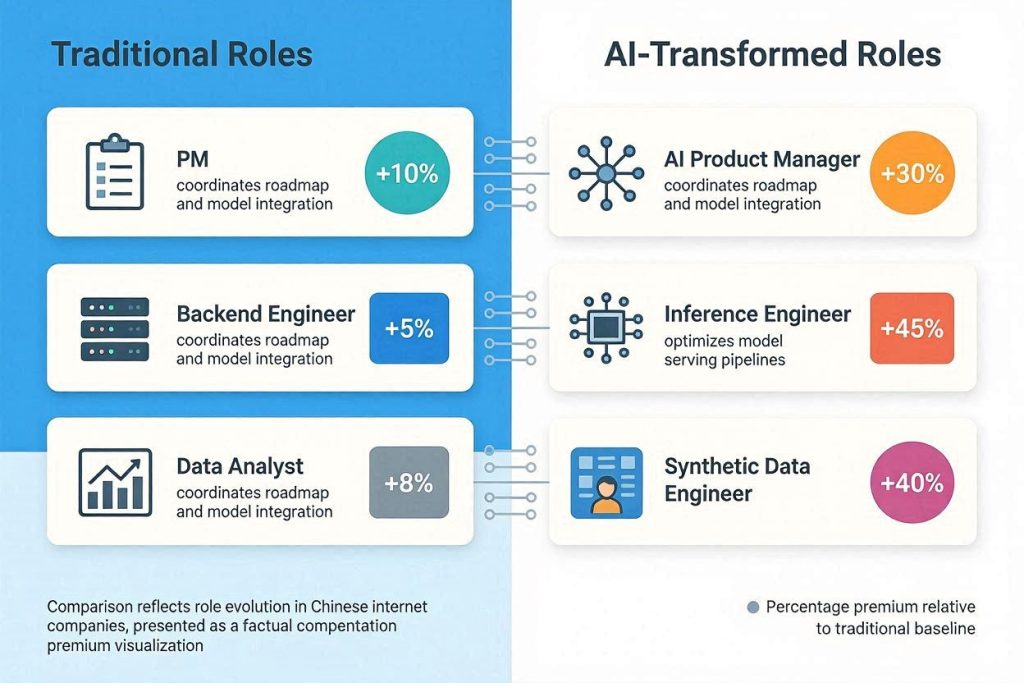

| Dimension | Traditional Role | AI-Transformed Role | Premium |

|---|---|---|---|

| Product | Product Manager | AI Product Manager (Prompt/LLM literacy) | +25%-35% |

| Engineering | Backend Engineer | AI Inference/Model Serving Engineer | +30%-45% |

| Algorithm | Recommendation Engineer | LLM Training / Fine-tuning / RLHF | +35%-55% |

| Data | Data Analyst | Data Labeling Strategy / Synthetic Data Engineer | +20%-30% |

Signal 3: "Containment Has Failed" — The Macro Talent Context

The Atlantic’s core argument — US technology curbs on China have limited effectiveness — has direct talent market implications:

- Overseas Chinese AI returnees accelerating: H1 2026 estimates suggest a 30%-40% YoY increase in returnees, driven by “more opportunity, faster deployment” in China’s AI sector.

- Cross-border compensation gap narrowing: For top-tier AI researchers, Chinese firms now offer 60%-70% of US-equivalent total comp (up from 40%-50% in 2022

Data Support China AI Core Roles — Quick Compensation Benchmark Early Q2 2026, Industry Estimates

Table 2: Compensation Benchmark| Role | P50 (CNY 10K/yr) | P75 (CNY 10K/yr) | YoY | Key Driver |

|---|---|---|---|---|

| LLM Training Engineer | 95 | 135 | +28% | Supercomputer/cluster demand |

| AI Inference Engineer | 72 | 105 | +32% | Super-app deployment pressure |

| AI Product Manager (LLM) | 68 | 92 | +25% | Product-layer AI integration |

| AI Chip Designer (HiSilicon) | 85 | 120 | +20% | Domestic substitution push |

| Compiler/Kernel Engineer | 78 | 115 | +30% | Homegrown compute stack |

| AI Research Scientist (PhD/Top Conf.) | 120 | 180 | +22% | Foundation model competition |

China AI Supercomputing Talent Gap Estimates

Table 3: Talent Gap| Specialization | Current Headcount | Estimated Gap | Difficulty Index (1-10) |

|---|---|---|---|

| Large-Scale Distributed Training | 2,500-3,000 | 4,000-5,000 | 9 |

| AI Chip Architecture Design | 1,800-2,200 | 2,500-3,000 | 9 |

| Kernel Development (CUDA-compat) | 600-800 | 1,500-2,000 | 10 |

| Compiler Optimization (AI) | 800-1,000 | 2,000-2,500 | 9 |

Impact on HR

For Foreign-Employed HR Leaders in China

- Reassess your China AI team posture. Chinese AI talent is shifting from “cost center” to “technical capability center.” If your China R&D center hasn’t planned headcount for LLM training or inference optimization, recommend completing a 3-5 core position plan before Q3 2026 — the window is closing.

- Watch the “two-way flow” trend. Historically, foreign firms worried about losing talent to ByteDance/Tencent/Huawei. Now there’s a reverse flow — overseas Chinese AI talent returning to domestic firms. You can attract this group with a “global role + China compensation” package, especially for positions that interface with global HQ.

- Update your compensation benchmarks. The anchor point for AI talent has expanded from “big tech” to “compute infrastructure companies” (HiSilicon, Sugon, BirenTech, etc.). Recommend benchmarking to at least the P75 level for AI infrastructure roles.

For Domestic HR Leaders and Founders

- “Compute talent” is the new scarce species. Hardware engineering, system software stack, kernel development — these non-algorithm roles will be harder to hire than algorithm roles by H2 2026. Start sourcing compiler and distributed systems candidates now, even if you don’t need them today — you will in 6 months.

- Super-app AI hiring creates a talent cascade. Tencent, ByteDance, and Meituan are absorbing massive AI talent externally. If you’re not tier-1, target the mid-level talent that tier-1 companies leave behind after their raiding — they have real experience but aren’t “top conference” stars, and offer exceptional value.

- Rethink equity/comp design. Chinese AI startups are experimenting with “compute resource equity” — granting A100/H100 access as part of compensation. Consider adding this dimension to your comp architecture as a differentiation tool.